What will life be like if CPF is never implemented?

-

Originally posted by sgdiehard:

CPF implemented in 1980s?

"Singapore introduced CPF as early as 1955 as compulsory savings scheme for retirement. In the 70s CPF contributions were increased to cushion rising inflation,......

no difference between renting and buying? when you buy the house its yours, 30 years or sooner, and you can pass on to your children. Your really have a roof. and if prices are high and you sell, you pocket the difference, then you can buy a smaller one, move to the lowest priced district, or move to live with your children, ..

when you rent you, the house is never yours... good that you can be happy to just rent, or it is the affordability that matters?

don't need statistics to compare HK, just talk to the people there. Cannot build houses on hills, the ones at the mid level are the most expensive ones, private properties, guess why?

If you choose what you want to read, any other info I guess it would be futile.

My bad! I thought MRT construction began in 1980s, that why they implemented the CPF in 1980s, I was wrong. The CPF was implemented in 1970s in order for the government to control inflation during the construction of MRT from 1970s to 1980s.

So now you agree with me that CPF was used by the government to control inflation during the construction of MRT?

What about your contention that Hong Kong has a bigger area for development?

You seem to have omitted my questions in an earlier post.

You mean to tell me in the past, housing was built for the benefit of foreigners to purchase? You sure about your claims?

Housing for foreigners was just a small percentage in the past, but within these few years, with the governmen't policy of increasing citizens by importing foreigners has led to a drastic increase in the price of properties. (1.5 million foreigners compare to 3 million citizens {also take note that some of these 3 million citizens are newly converted foreigners}) That's why I said, in the past housing was more of an internal growth, but these past few years, with a steep increase in population (by immigration from PRC, India, Indonesia), the price of housing has increased more drastically. If you have problems understanding this, just go to the Singstat website to confirm that Singapore's population has increased substantially these few years. 12 year cycle? Maybe you can cite the source of your theory? So when is the peak and trough of this 12 year cycle? What 3.5% investment in private housing are you talking about? You sure you understood all my post?

You obviously have problems understanding what is the $60,000 cap in CPF. Way to go captain obvious!

For stating that when you rent the house, it doesn't belong to you. There are significant difference between renting and buying in Hong Kong, but this obviously doesn't happen here because government doesn't subsidise you for the cost of housing when you rent. Can you purchase a 80 sq. m. flat for SG$522 a month in Hong Kong? Everything about the PAP government is about deriving profits from her citizens. -

When you talk about the 3.5% interest you are getting from the CPF Board being risk free, is totally bollocks.

Why? It's because CPF Board doesn't operate like any commercial banks. If there is a requirement to fulfill her needs for cash to meet CPF members, say Temasek and GIC have been making very bad investment decisions that resulted in more losses (that reserves have dwindled to nothing or negative), to meet the cash requirement of CPF members withdrawal MAS could always print more money. With extra money flooding the market, inflation would rise, reducing the value of your money.

The 3.5% interest rate does not protect CPF members from inflation risk, a risk that is CPF members take with the Singapore currency (you live in Singapore and you only use SG$), but they are not paid for the inflation risk that they take. A good example will be the recent 4-5% inflation, while CPF still pays you 3.5%.

A fairer distribution would be inflation linked interest rates, say 6% (interest rate) + inflation rate, 3.5% interest is exploitative.

-

Originally posted by deepak.c:

You sure you got your 4 Room HDB for $112,000?

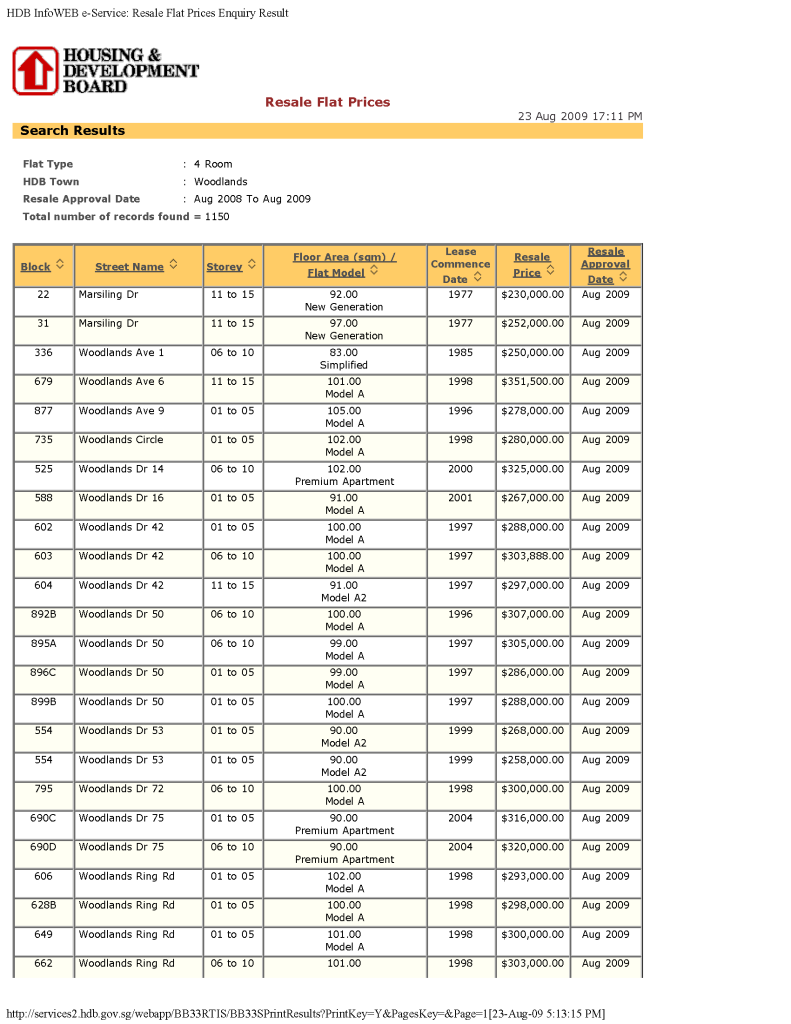

I would be scared living in there, it might be the haunted, that's why owners are letting it go cheap, the current resale prices of 4 Room HDB ranges from $230,000 to $351,500.

I wonder if you pay $460 a month, will you complete paying for your 4 Room HDB in 100 years.

Not possible, you would need to pay $562 a month in order to pay up your $230,000 4 Room HDB in 100 years.

Yes.... $112K.... 10years ago. And Not resale but 1st timer..... $112K doesn't include the money I paid to HDB with whats in my CPF ($32K if I remember). My loan was only $80++ K. Btw..... making tastless joke wouldn't change the fact that you guess wrong.

-

Originally posted by hloc:

Yes.... $112K.... 10years ago. And Not resale but 1st timer..... $112K doesn't include the money I paid to HDB with whats in my CPF ($32K if I remember). My loan was only $80++ K. Btw..... making tastless joke wouldn't change the fact that you guess wrong.

I surely didn't guess wrong. When people compare they usually talk about current figures, you use 10 years ago.

You might as well tell us 40 years ago when it was just $8,000 and you completed paying for your HDB in 1 year.

You add some amusement to a tense Speakers' Corner.

-

Originally posted by seyKai:

why u guys treating your money in the CPF like free money? other than buying overpriced HDB falts?

Or you could leave the money inside by NOT buying a House.... and hope that you would live long enough to collect it when you are 62.... or 63.... or 64..... or 65.... or 66.... or whenever Govt decide you 'Old' enough to get it.

I rather use my $$$ to buy house (over price or otherwise) than leave it inside CPF. Overprice - I still got roof over my head. Not Overprice - I still got roof over my head. Downgrade - I still can get cash after returning part of the $$$ into my CPF. Leave it in CPF totally don't use - Can only hope that I would get it before I die.....

Which do you think is better..... Use or Don't Use

-

Originally posted by deepak.c:

I surely didn't guess wrong. When people compare they usually talk about current figures, you use 10 years ago.

You might as well tell us 40 years ago when it was just $8,000 and you completed paying for your HDB in 1 year.

You add some amusement to a tense Speakers' Corner.

Doesn't change the facts that I got my house with CPF and will be making a profit (last time agent called.... buyer willing to pay $185K

) if I rent out / downgrade.Moral of the story..... buy your house while you are still young and can take a long loan.... instead of KPKB about price then get into the market too late. No bank is willing to give you a long loan if you already 40+.....

Btw... my parents brought their 3Room HDB at AMK 30years ago at $65+ K..... while $65K isn't much today..... 30years ago, its alot of $$$. Before they move in with me at my new place in Woodlands 10years ago.... they sold that $65+ K unit for $150+K..... Your little update of HDB flat prices stated that my Woodlands area for resale is worth at about $300K..... Wow, 10years and already $100++K extra

So deepak.c .... if you buy as 1st timer..... for, lets said $200K..... what would the price be 10years from now

So deepak.c .... if you buy as 1st timer..... for, lets said $200K..... what would the price be 10years from now  FYI..... don't buy a flat and think you will make $$$ in 6mths time, its for the long haul.....

FYI..... don't buy a flat and think you will make $$$ in 6mths time, its for the long haul..... And why should Speaker Corner be tense.....

You could said as much as you want here..... give as much good points as you can.... and at the end of the day.... - It Will Still Be The Same Tomorrow Morning - .... believing that the system will change just because you wrote in SG Forum is where the REAL amusement begins..... -

Originally posted by hloc:

Doesn't change the facts that I got my house with CPF and will be making a profit (last time agent called.... buyer willing to pay $185K

) if I rent out / downgrade.Moral of the story..... buy your house while you are still young and can take a long loan.... instead of KPKB about price then get into the market too late. No bank is willing to give you a long loan if you already 40+.....

Btw... my parents brought their 3Room HDB at AMK 30years ago at $65+ K..... while $65K isn't much today..... 30years ago, its alot of $$$. Before they move in with me at my new place in Woodlands 10years ago.... they sold that $65+ K unit for $150+K..... Your little update of HDB flat prices stated that my Woodlands area for resale is worth at about $300K..... Wow, 10years and already $100++K extra

So deepak.c .... if you buy as 1st timer..... for, lets said $200K..... what would the price be 10years from now FYI..... don't buy a flat and think you will make $$$ in 6mths time, its for the long haul..... And why should Speaker Corner be tense.....

You could said as much as you want here..... give as much good points as you can.... and at the end of the day.... - It Will Still Be The Same Tomorrow Morning - .... believing that the system will change just because you wrote in SG Forum is where the REAL amusement begins..... When you friend talk about how the price of kopi-o has increased so much these few years. Do you go around telling them that it's $0.40? Then tell them that that was 10 years ago.

I am so sad that I don't have a HDB to call my own and I am so envious of your 4 Room HDB.

I like your assumptions, like all assumptions is a basis of fubar.

Another failed assumption and belief. "And why should Speaker Corner be tense.....

You could said as much as you want here..... give as much good points as you can.... and at the end of the day.... - It Will Still Be The Same Tomorrow Morning - .... believing that the system will change just because you wrote in SG Forum is where the REAL amusement begins..... "So you admit that my points are good. I can't say the same for your "I bought my 4 Room HDB at $112k, therefore housing is cheap TODAY".

Ermm......Who is believing that they system will or will not change? I made no such claims, my posting is to educate you and other uninitiated the fallacies of their assumptions.

I will continue to post so long as I see that any statements is fallacious. -

Originally posted by deepak.c:

When you friend talk about how the price of kopi-o has increased so much these few years. Do you go around telling them that it's $0.40? Then tell them that that was 10 years ago.

I am so sad that I don't have a HDB to call my own and I am so envious of your 4 Room HDB.

I like your assumptions, like all assumptions is a basis of fubar.

Another failed assumption and belief.

"And why should Speaker Corner be tense.....

You could said as much as you want here.....

give as much good points as you can.... and at the end of the

day.... - It Will Still Be The Same Tomorrow Morning

- .... believing that the system will change just because

you wrote in SG Forum is where the REAL amusement begins.....

"So you admit that my points are good. I can't say the same for your "I bought my 4 Room HDB at $112k, therefore housing is cheap TODAY".

Ermm......Who is believing that they system will or will not change? I made no such claims, my posting is to educate you and other uninitiated the fallacies of their assumptions.

I will continue to post so long as I see

that any statements is fallacious.Whatever Bro..... don't buy, contiune to rent, die die don't leave your parent's house... hope against hope that prices will becomes dirt cheap..... it is YOU who will have to decide for yourself. While you DID have some good points.... SO DID EVERYONE ELSE, incase you didn't notice

.... but if you need to 'win'.... ok lor And thxs again for updating me that my unit is now worth around $300K..... next time agent called, at least I know it will be worth more than the $185K they quote me at the end of last year

-

Originally posted by hloc:

Whatever Bro..... don't buy, contiune to rent, die die don't leave your parent's house... hope against hope that prices will becomes dirt cheap..... it is YOU who will have to decide for yourself. While you DID have some good points.... SO DID EVERYONE ELSE, incase you didn't notice

.... but if you need to 'win'.... ok lor And thxs again for updating me that my unit is now worth around $300K..... next time agent called, at least I know it will be worth more than the $185K they quote me at the end of last year

Yes. I will continue to rent and die die don't leave parents house and hope against hope that prices will becomes dirt cheap.

Seriously, if you need me to update you on simple things such as the price of 4 Rooms HDB in Woodlands, something is very wrong.

And you think that every unit sells for $300k.

-

Originally posted by hloc:

Or you could leave the money inside by NOT buying a House.... and hope that you would live long enough to collect it when you are 62.... or 63.... or 64..... or 65.... or 66.... or whenever Govt decide you 'Old' enough to get it.

I rather use my $$$ to buy house (over price or otherwise) than leave it inside CPF. Overprice - I still got roof over my head. Not Overprice - I still got roof over my head. Downgrade - I still can get cash after returning part of the $$$ into my CPF. Leave it in CPF totally don't use - Can only hope that I would get it before I die.....

Which do you think is better..... Use or Don't Use

hloc,

I agree that if you are given a choice to use either cash or cpf to pay for your roof over your head, using CPF is a no brainer lah.

Unless you intend to sell your flat and not purchase another one , then ofcors you pocket the appreciated value 100%.

However, you sell your home at $y psf, but needs to purchase another smaller unit at $Y+X psf ( X being inflation ), plus new interest you need to tag on to the new purchase. How can that be worth it at all ?

As long as you go from a bigger to smaller floor area, there's already a saving in price difference. So how is this really a gain ?

If HDB don't reign in the price of flats , newer generations will no longer be able to afford one for their family.

But older generations like you , will be angry if HDB does lower the price as it will affect the value of your HDB lease resale.

Now how can that be good ?

Older generations wants to make big profit from HDB, newer generations needs affordable housing.

Who's gonna give ?

Having your boss pay into your CPF is not something you ought to be so found of , really.

In their books, CPF payment is an expense/labour cost anyway.

The difference is, they need to pay into the CPF and limit what you can do with the money, instead of paying it to your pocket so you can decide for yourself what you want to use it for.

Personally, I do prefer my boss give me the 20% directly, instead of to the CPF. Unfortunately, in Singapore, we don't have a choice.

-

Originally posted by jojobeach:

hloc,

I agree that if you are given a choice to use either cash or cpf to pay for your roof over your head, using CPF is a no brainer lah.

Unless you intend to sell your flat and not purchase another one , then ofcors you pocket the appreciated value 100%.

However, you sell your home at $y psf, but needs to purchase another smaller unit at $Y+X psf ( X being inflation ), plus new interest you need to tag on to the new purchase. How can that be worth it at all ?

As long as you go from a bigger to smaller floor area, there's already a saving in price difference. So how is this really a gain ?

If HDB don't reign in the price of flats , newer generations will no longer be able to afford one for their family.

But older generations like you , will be angry if HDB does lower the price as it will affect the value of your HDB lease.

Now how can that be good ?

Older generations wants to make big profit from HDB, newer generations needs affordable housing.

Who's gonna give ?

Having your boss pay into your CPF is not something you ought to be so found of , really.

In their books, CPF payment is an expense/labour cost anyway.

The difference is, they need to pay into the CPF and limit what you can do with the money, instead of paying it to your pocket so you can decide for yourself what you want to use it for.

Personally, I do prefer my boss give me the 20% directly, instead of to the CPF. Unfortunately, in Singapore, we don't have a choice.

Many think that downgrading will earn money, but you must also understand that you are getting a lesser asset, some who are paying interest for their 5 rooms downgraded to 4 rooms and use the profit to clear off all his loan for the leasing. Then they proclaim that they are loan free..like very happy. Well, to me, firstly you get a smaller rooms with lower asset value, and secondly, after paying for the 5 rooms for some years with the initial downpayment, you offload it to get a 4 rooms with all profits channelled to get a loan free condition, you are actually paying a very high cost and in the end get a rooms of what you initially wanted. Now you understand why HDB wants occupants to stay in new flats for a few years before they can sell. I do not exactly know the nos of years as i dun live in HDB, if let say 5 years, with the initial downpayment and 5 years of paying loan+interest, all these will be gone..in HDB coffer.

Unless u want to gain completely, as above said, no more buying, either you sleep at our well designed bus-stops or East coast Park with tents and BBQ and a full sea view.

-

I have heard of cam whoring, but forum whoring?

-

huh?..u too much whoring liao,..must be

-

Originally posted by angel7030:

Many think that downgrading will earn money, but you must also understand that you are getting a lesser asset, some who are paying interest for their 5 rooms downgraded to 4 rooms and use the profit to clear off all his loan for the leasing. Then they proclaim that they are loan free..like very happy. Well, to me, firstly you get a smaller rooms with lower asset value, and secondly, after paying for the 5 rooms for some years with the initial downpayment, you offload it to get a 4 rooms with all profits channelled to get a loan free condition, you are actually paying a very high cost and in the end get a rooms of what you initially wanted. Now you understand why HDB wants occupants to stay in new flats for a few years before they can sell. I do not exactly know the nos of years as i dun live in HDB, if let say 5 years, with the initial downpayment and 5 years of paying loan+interest, all these will be gone..in HDB coffer.

Unless u want to gain completely, as above said, no more buying, either you sleep at our well designed bus-stops or East coast Park with tents and BBQ and a full sea view.

Obviously the males in this forums think otherwise.. or they prefer to lie to themselves they are making big money.... LOL !!!

The HDB resale market is a fluke, but so many Singaproeans/PRs are buying into it. Paying a much higher price on a shorter lease.

And new HDB value goes up, because people think they can make a bundle upon resale thus are so willing to pay for sky high prices.

In the end, people are just screwing each other over. In the long term, everyone has come to accept this is how it is in Singapore.

I'd rather see HDB re-possess lease than have it go into resale by lease owners. Then re-lease it to applicants to keep a tab on prices.

-

Originally posted by jojobeach:

Obviously the males in this forums think otherwise.. or they prefer to lie to themselves they are making big money.... LOL !!!

The HDB resale market is a fluke, but so many Singaproeans/PRs are buying into it. Paying a much higher price on a shorter lease.

And new HDB value goes up, because people think they can make a bundle upon resale thus are so willing to pay for sky high prices.

In the end, people are just screwing each other over. In the long term, everyone has come to accept this is how it is in Singapore.

I'd rather see HDB re-possess lease than have it go into resale by lease owners. Then re-lease it to applicants to keep a tab on prices.

They are just being used by the govt HDB policies, good for housing agents too, HDB executives dun hold top meeting just to sing song and talk cock, they are finding way to take as much as possible from you and yet they can make it in a way of delighting you. Resale/upgrading and downgrading is a good business for both govt and agents.

Likewise, if you looks at how peoples make money without even the private house/condo being built, you will find HDB is completely a scam in term of resale/upgrade/downgrade is concern. At the end of the day, in HDB, no matter if you upgrade or downgrade, you fall into the decision makers plan. But what to do, peoples are like that, they feel loan free,,,but never see the amount they paid and the smaller asset they get. Sad

-

Originally posted by angel7030:

They are just being used by the govt HDB policies, good for housing agents too, HDB executives dun hold top meeting just to sing song and talk cock, they are finding way to take as much as possible from you and yet they can make it in a way of delighting you. Resale/upgrading and downgrading is a good business for both govt and agents.

Likewise, if you looks at how peoples make money without even the private house/condo being built, you will find HDB is completely a scam in term of resale/upgrade/downgrade is concern. At the end of the day, in HDB, no matter if you upgrade or downgrade, you fall into the decision makers plan. But what to do, peoples are like that, they feel loan free,,,but never see the amount they paid and the smaller asset they get. Sad

Sad indeed. We're paying them million lollars to screw us over....

Score - Elite 1 : Heartlanders 0

-

Originally posted by jojobeach:

Sad indeed. We're paying them million lollars to screw us over....

what to do, they like to get screwed..buy a HDB flat is ok,..but to get further screwed by upgrading and downgrading stuffs, is totally open screwing.People upgrading have many reasons, to show off, a bigger family, get rich etc etc..i suggest they upgrade to private properties if you really want to upgrade, if not you are still inside the HBD wheels of fortune.

People downgrade talk big about loan free and bigger room hard to clean, but actually, most are in heavy debts, medical debts and or simply cannot sustain the loan+interest with lost of jobs etc etc

-

Baby boomer generation + CPF implementation = Big mass of mess for everyone

Right?

-

It seems that you guys/gals don't own a House and don't understand how its done..... let me explain.

My house brought at $112K..... will I sell just because 'Market' is good. ?? - No.

Why -

Because I don't intend to get into 'New' debt (new loan with new interest... etc)

Because that is my HOME.... NOT an Investment like Shares in the Stock Market. (you just don't Buy Sell Buy Sell for fun)

But I will sell it WHEN -

My childrens are all grown up and leaves the house (need not so much room)

When I retire and could use the extra cash along with my CPF.

Downgrade -

If my new smaller until is expensive due to inflation.... wouldn't you said that my 4Room would also worth more due to Inflation ?? Or do you think that only one side got inflation while the other won't ??

Example - If I'm to retire NOW (House already Fully paid for).... FYI, my loan will finish before I hit 55... I did my MATH before I buy

Accounting to deepak.c update on HDB price of resale 4Room flat in Woodlands area.... My flat would be worth $300K +/-..... A resale 3Room flat in Woodlands is selling on the avg of $190-205K NOW... (go to HDB Resale and click 3Rooms Woodlands from Jan to Aug 2009)

So... $300K - $200K = $100K +/-

Since I don't need any more loan.... it will be pure cash (after agent & Govt take their shares lah)

And I wouldn't even need a 3Room..... because only me and the Wife would be living there.... and since I never did believe that I would live till 80 anyway.... I will most likely apply for those very small Studio Apartment for Seniors.... You get a 30year lease for perhars $60K (I think deepak.c will update me the price soon) but Govt will take back the flat once you are dead... as you DON'T own the until.....

But who cares...... at the most will live another 20years after leasing the House only anyway.

FYI..... if younger S'porean can't afford to buy house NOW..... do anyone here think it was 'EASY' for me 10years ago ?? My House might seems 'Cheap' now when compare to the price today... but it wasn't 'CHEAP' 10years back.... Don't forget, Inflation was around 10years ago too. If deepak.c wants to said 40years ago House is only $8000.... do deepak.c knows how many people have $8000 back then ?? Yeah yeah... my $112K House is CHEAP.... do you think I would need a 30years loan if it was CHEAP then ?? Use your BRAIN lah.... When my Parents was working 40years ago... basic pay was $500+. My time - $1200+.... nowadays.... No young S'porean from poly would work for anything less than $1600-1800....

So.... how you want to compare long time ago.....

-

Originally posted by Dejomel:

Baby boomer generation + CPF implementation = Big mass of mess for everyone

Right?

Left.It all depend on how your sow your seeds.

-

Use your BRAIN lah.... When my Parents was working 40years ago... (HBD-$8000)basic pay was $500+. My time - $1200+ (HDB $112,000).... nowadays.... No young S'porean from poly would work for anything less than $1600-1800.... (2009-HDB $300,000 )

I think u should be the 1 who need to use your brain in calculation

-

Originally posted by hloc:

It seems that you guys/gals don't own a House and don't understand how its done..... let me explain.

My house brought at $112K..... will I sell just because 'Market' is good. ?? - No.

Why -

Because I don't intend to get into 'New' debt (new loan with new interest... etc)

Because that is my HOME.... NOT an Investment like Shares in the Stock Market. (you just don't Buy Sell Buy Sell for fun)

But I will sell it WHEN -

My childrens are all grown up and leaves the house (need not so much room)

When I retire and could use the extra cash along with my CPF.

Downgrade -

If my new smaller until is expensive due to inflation.... wouldn't you said that my 4Room would also worth more due to Inflation ?? Or do you think that only one side got inflation while the other won't ??

Example - If I'm to retire NOW (House already Fully paid for).... FYI, my loan will finish before I hit 55... I did my MATH before I buy

Accounting to deepak.c update on HDB price of resale 4Room flat in Woodlands area.... My flat would be worth $300K +/-..... A resale 3Room flat in Woodlands is selling on the avg of $190-205K NOW... (go to HDB Resale and click 3Rooms Woodlands from Jan to Aug 2009)

So... $300K - $200K = $100K +/-

Since I don't need any more loan.... it will be pure cash (after agent & Govt take their shares lah)

And I wouldn't even need a 3Room..... because only me and the Wife would be living there.... and since I never did believe that I would live till 80 anyway.... I will most likely apply for those very small Studio Apartment for Seniors.... You get a 30year lease for perhars $60K (I think deepak.c will update me the price soon) but Govt will take back the flat once you are dead... as you DON'T own the until.....

But who cares...... at the most will live another 20years after leasing the House only anyway.

FYI..... if younger S'porean can't afford to buy house NOW..... do anyone here think it was 'EASY' for me 10years ago ?? My House might seems 'Cheap' now when compare to the price today... but it wasn't 'CHEAP' 10years back.... Don't forget, Inflation was around 10years ago too. If deepak.c wants to said 40years ago House is only $8000.... do deepak.c knows how many people have $8000 back then ?? Yeah yeah... my $112K House is CHEAP.... do you think I would need a 30years loan if it was CHEAP then ?? Use your BRAIN lah.... When my Parents was working 40years ago... basic pay was $500+. My time - $1200+.... nowadays.... No young S'porean from poly would work for anything less than $1600-1800....

So.... how you want to compare long time ago.....

hi,

first and foremost, when you buy a govt HDB flat, u dun need to do your math and calculate the loan, they will be calculating for you free of charge. A built in service.

Secondly, what is 100k today in comparing to 10 years ago? If you had lived there for 10 years ++, how much have you paid already inorder to maintain the loan cum interest + initial downpayment.

And at that time of your initial purchase, if you paid 30k with CPF, it is equivalent to 50 to 70k now in term of inflation. Add your monthly payment, you could have paid more than 112k now, with the govt already earn your first part, now they are looking forward to your second part. And if you downgrade, you get a 3 rooms with foreign workers quarters, poor PR peoples, poor lift hygience, plus have to paid $200k++ add your former 4 rooms you paid 112k++, in the end, you paid 312k++ living in a 3 rooms after nearly all your life of working like slave

-

Originally posted by seyKai:

Use your BRAIN lah.... When my Parents was working 40years ago... (HBD-$8000)basic pay was $500+. My time - $1200+.... nowadays.... No young S'porean from poly would work for anything less than $1600-1800.... (2009-HDB $300,000 )

I think u should be the 1 who need to use your brain in calculation

Remembered 40 years or more ago landed properties also not that expensive. A single terrace1,600 sq ft was $10,000 compared to a 3 room HDB $8,000.

-

Originally posted by angel7030:

hi,

first and foremost, when you buy a govt HDB flat, u dun need to do your math and calculate the loan, they will be calculating for you free of charge. A built in service.

Secondly, what is 100k today in comparing to 10 years ago? If you had lived there for 10 years ++, how much have you paid already inorder to maintain the loan cum interest + initial downpayment.

And at that time of your initial purchase, if you paid 30k with CPF, it is equivalent to 50 to 70k now in term of inflation. Add your monthly payment, you could have paid more than 112k now, with the govt already earn your first part, now they are looking forward to your second part. And if you downgrade, you get a 3 rooms with foreign workers quarters, poor PR peoples, poor lift hygience, plus have to paid $200k++ add your former 4 rooms you paid 112k++, in the end, you paid 312k++ living in a 3 rooms after nearly all your life of working like slave

Wao Liao..... Don't you know the I meant making sure that I would finish payment before 55 ??!! Don't you know that if you finish payment by 55, you could use the half the price of your flat as part of the CPF condition (at least 120K inside) to withdraw half of your CPF money out (the rest of your money at 62.... for now).

30K is equivalent to 50-70K... u sure or not ?? Again don't you understand that I was trying to inform you that it was a big headache for me to pay out 30K then as it is like you to pay out 50-70K now.....

And don't you understand that my loan of 88+K at $460+ a month DOES NOT CHANGE EVEN WITH INFLATION ?? I will pay $460 a month from 10years ago, till today, and untill the loan is over and yet my flat is already worth more than what I agreed to paid for..... and for crying out loud.... Do you think Banks are into the business of giving you an Interest Free installment..... Get Real.... Ah Long also charge you 20% interest for 6 weeks.

And which part of - HOUSE ALREADY FULLY PAID FOR - do you NOT understand ??

But I will sell it WHEN -

My childrens are all grown up and leaves the house (need not so much room)

When I retire and could use the extra cash along with my CPF.

Example - If I'm to retire NOW (House already Fully paid for).... FYI, my loan will finish before I hit 55... I did my MATH before I buy

and how in world did you came out with 312K ??

I buy house at $112K (which I work to pay for)

I sold house at $300K (Profit of $188K)

I now have $300K without a house.... but neither do I owe the bank/hdb/CPF anything because its already paid for after the 30year loan...

I buy new house...... $300K - $200K = $100K of cash for myself. Even if I have to pay back CPF $32K.... that is still $68K. And did I mention that it is when I retired and is taking my CPF at age 55....... the $32K will still be given half to me....

And most importantly - NO LOAN TO REPAY.....

And that is IF I BUY A 3Room flat instead of a cheaper Studio Apartment like I said I would most likely do.....

-

Originally posted by seyKai:

Use your BRAIN lah.... When my Parents was working 40years ago... (HBD-$8000)basic pay was $500+. My time - $1200+ (HDB $112,000).... nowadays.... No young S'porean from poly would work for anything less than $1600-1800.... (2009-HDB $300,000 )

I think u should be the 1 who need to use your brain in calculation

Yes... you DID NOT use your brain.....

1st - that quote was to highlight that as your pay increase.... so did the cost of the Flat.... that is call 'Inflation'.....

2nd - The 2009 HDB of $300K is because you are buying RESALE Flat instead of buying New Flat. A schoolmate of mine is getting his flat in 2011 near the S'pore Sport School in Woodlands at $186+K. Therefore, if you don't have the $$$$..... buy and then wait for newly built flats (2-3years to complete) instead of die die also want to buy resale at mature housing estate like AMK, Yishun, Toa Payoh...etc. Mature Estate will always cost more than new estate like Sengkang....